Copperlane

Turn hours of loan processing into seconds

349 followers

Turn hours of loan processing into seconds

349 followers

Copperlane is an AI-native loan origination system. Our AI agent, Penny, optimizes rate pricing, guides borrowers, and verifies documents - cutting loan processing time from hours to seconds.

Copperlane

Hey PH! I’m Brianna, co-founder of Copperlane (YC W26)!

The Problem

Lenders spend $11,800 to originate a mortgage, and the majority of that cost is burned during intake due to missing documents, back-and-forth, and costly errors. This manual process breaks down on almost every loan, across 8 million loans a year.

Existing tools fall into two approaches:

❌ Legacy portals – These systems are decades old, and loan officers need to chase down borrowers for docs manually.

❌ AI built by older mortgage teams – Our competitors are all mortgage people trying to build AI. We’re the only AI people learning about and building for mortgage. :)

My co-founder and I both come from mortgage families (Freddie, Fannie, FHA), so the space is personal to us and we built Copperlane to fix it.

How Copperlane is Different 🚀

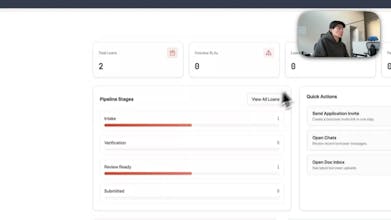

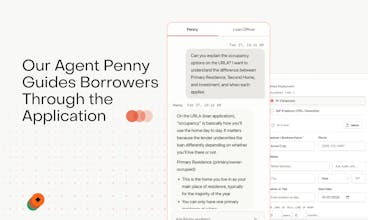

Copperlane is an AI-native loan origination system powered by our agent, Penny, who behaves like a real loan officer.

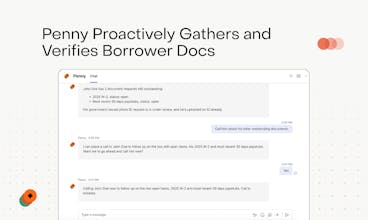

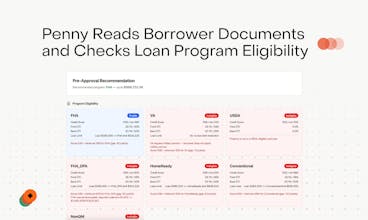

🔸 Penny handles intake proactively – She pulls borrower docs, reads them, and checks the borrower’s loan eligibility.

🔸 Guides borrowers through the application – Penny answers questions and proactively helps borrowers complete the loan application correctly.

🔸 Proactively fixes issues – Is the borrower missing a paystub? Or reported conflicting income? Penny flags it immediately and follows up with the borrower.

🔸 Delivers clean files to lenders – Loan officers receive clear, organized files and can focus on bringing in new loans.

Who this is for

If you’re a lender or loan officer dealing with slow intake, Penny helps you close loans faster without extra headcount.

📎 Get started today

We’d love to show you what Penny can do! You can book a demo at here.

Carpe Diem,

– Brianna & Athan

@brianna_lin Hi Briana, indeed this was a long term waiting on filling the gaps from the underwriting side to handle complex paperwork. I am a business advisor and work with lots of lenders in SBA 7a and conventional loans. Is your model strictly for residential mortgages or can it be utilized for business or commercial properties?

Copperlane

@amir_dawdani Hey! We're primarily focused on mortgages/residential at the moment, but are open to exploring commercial loans in the future.

The document verification piece is what catches my attention — that's historically been the biggest bottleneck in loan processing, not the rate calculation. Curious how Penny handles edge cases like inconsistent income documentation for self-employed borrowers, that's usually where automated systems fall apart and a human has to step back in. If you've solved that reliably this could be genuinely transformative for smaller lenders who can't afford large underwriting teams.

Copperlane

@zerodarkhub Hey! Great question, so Penny flags inconsistencies across documents (like mismatched income signals) and surfaces them with clear explanations so loan officers can quickly review edge cases.

Told

Curious how Penny handles edge cases — like when a borrower’s docs are inconsistent or their situation doesn’t fit a standard risk profile. That’s usually where loan processing actually breaks down, not in the straightforward cases. The ‘hours to seconds’ promise is compelling but I’d want to know if the AI is making final calls or just surfacing recommendations for underwriters. The trust gap between ‘AI helped’ and ‘AI decided’ is massive in lending specifically.

Copperlane

@jscanzi Hey! So Penny doesn’t make credit decisions. It's main job is to flag inconsistencies, ask borrowers follow-up questions, and surface issues early so underwriters receive a clean file to review. The idea is that the loan office doesn't need to spend time doing any loan closing manually, so they can focus solely on bringing in new borrowers.

Told

@brianna_lin Thank you for your answer!

The "AI people learning mortgage" vs "mortgage people trying to build AI" framing is sharp and honest. Having Penny proactively flag issues like missing paystubs instead of waiting for a loan officer to catch it manually is where the real time savings happen. Congrats on YC W26, Brianna and Athan.

Copperlane

@siddhant_khurana Appreciate that! That’s exactly the idea behind Penny -- catching issues like missing paystubs early and keeping the file clean so loan officers don’t have to hunt through documents later.

How does Penny handle complex or non-standard borrower scenarios, such as self-employment income or inconsistent documentation, while ensuring full compliance with mortgage lending regulations?

Copperlane

@mordrag Hey Denis! So Penny flags things like self-employment income or inconsistent docs early, asks the borrower for the right supporting documents, and organizes everything for the loan team so underwriting gets a clean/compliant file.

In your lending workflow, which stage did you automate first (doc intake, pre-underwriting, risk checks, or pre-disbursement review)? And what explainability fields do you surface for human reviewers at each stage?

Copperlane

@hanxl We started with doc intake and borrower guidance in the point-of-sale system. Penny surfaces structured borrower data plus flagged inconsistencies so ops teams and underwriters can quickly review and verify.

Vela

This is pretty damn cool. How did you guys land on this idea?

Copperlane

@gobhanu_korisepati Thanks!! Athan and I's parent both work in the mortgage space so we grew up around it and got to learn about it first hand from them.